Real estate debt has always been a valuable component of any portfolio; however, it is emerging as a viable solution to a wide array of investor concerns today. It’s a strategy that offers a range of benefits with attractive risk-adjusted returns across market cycles.

Read our six reasons why investors should consider adding it to their portfolios, and learn more about our capabilities in Europe and the United States below.

1. Attractive risk-adjusted returns: In today’s environment, the combination of elevated interest rates and attractive credit spreads mean that real estate debt offers compelling returns relative to other fixed income alternatives. The potential for achieving these higher yields, while maintaining a relatively conservative risk profile, is appealing to institutional investors looking to mitigate risk.

Real estate debt can offer different opportunities through the market cycle, with the ability to adjust advance rates during market downturns to minimize risk, while benefiting from cyclical recoveries.

2. Stable and predictable income: An allocation to real estate debt may allow investors to enhance their portfolio income returns. The coupon-like nature of interest payments from borrowers can provide consistent and stable cash flows for investors, with a significant portion of the total return being achieved through income returns.

3. Downside protection and capital preservation: Real estate debt offers the ability for investors to gain exposure to the same underlying real estate, but via a protected position in the capital structure, offering an often-significant equity cushion to buffer against potential value fluctuations.

Careful structuring can further enhance downside protections; these investments are typically collateralized by the physical underlying property, providing security that differs to some other forms of fixed income investments. In a default event, active asset management is critical, and managers who have the expertise to step in and manage the underlying asset can further protect against potential losses and in some instances create upside value.

Senior or unlevered whole loan lenders sit in the last-loss position, allowing investors to consider more actively managed business plans than they might be comfortable investing in via an equity commitment.

4. Diversification benefits: Real estate debt provides exposure to one of the largest segments of the real estate market, typically with lower volatility than real estate equity. And adding real estate debt to an institutional portfolio can enhance diversification, as it often has low correlation with traditional asset classes like stocks and bonds, which can help to improve overall risk-adjusted returns.

5. Regulatory efficiency and opportunity: For insurance companies, real estate debt is treated favorably under Solvency II and other similar regimes, making it a capital-efficient way to deploy assets and capture attractive relative returns. Additionally, enhanced regulation has led to retrenchment by traditional bank lenders, creating opportunities for investors working with non-bank alternative lenders, such as institutionally managed debt funds.

6. Inflation hedge: As inflation rises, so too do the interest rates central banks often use to combat it. Real estate debt investments, particularly those with floating-rate loans linked to central bank rates, can therefore offer some protection against inflation.

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment. LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance. By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

This article first appeared in a Real Estate Debt special report in the February 2025 issue of Private Debt Investor (subscription required to read the full issue).

LaSalle’s David White and Craig Oram provide insights on navigating the evolving real estate debt markets in the US and Europe. They discuss the risk-adjusted returns that debt investments offer compared to equity, emphasizing steady returns and favorable lending conditions driven by recent market changes. They also share LaSalle’s strategic focus on scalable opportunities and underutilized assets, with a significant emphasis on the for-rent residential sector in the US.

This article first appeared in the Fall 2024 edition of PREA Quarterly

Chris Battista, Senior Product Manager at LaSalle Global Solutions, and Brian Klinksiek, Global Head of Research and Strategy, discuss the value of publicly traded real estate investments.

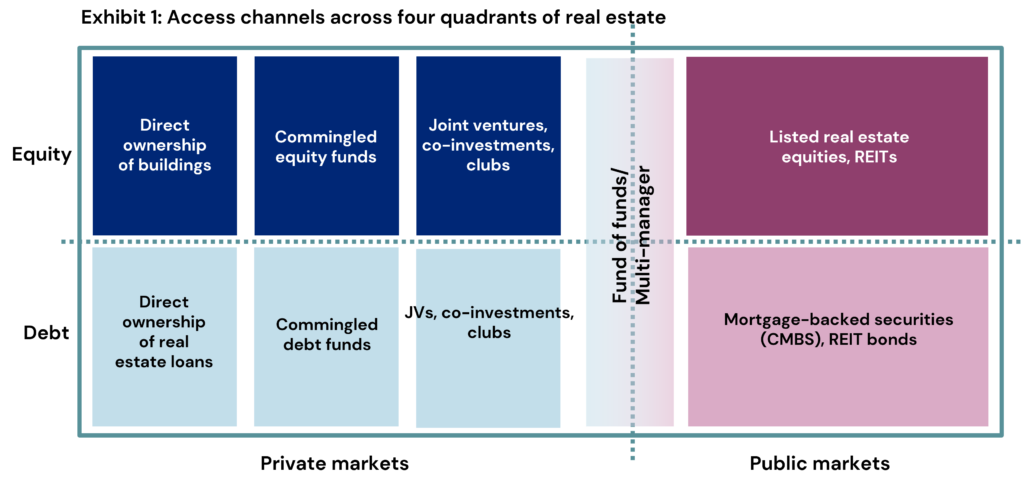

Investors should consider a holistic approach to the real estate asset class across the “four quadrants.” This means considering opportunities spanning both equity and debt positions on one dimension and both private and public market executions on the other (Exhibit 1). Doing so captures the full gross capitalization of real estate, enhances diversification, and opens opportunities to capture the best relative value. We call this being “quadrant smart” in LaSalle’s recently released ISA Portfolio View 2024, an annual report on portfolio construction.

Allocating between real estate debt and equity investing should be driven by risk appetite, views of relative pricing, and an investor’s broader portfolio considerations. Although debt investing has been quite topical over the past two years and covered by multiple investment managers, including LaSalle (see ISA Focus: Investing in Real Estate Debt), this article discusses the relationship between the public and private avenues to real estate equity investment.

Institutional investors tend to be well versed in private equity real estate investing but less consistent in their approach to the publicly traded side of real estate—even though the public side offers similar characteristics, a broad opportunity set, and often leading signals on the broader market’s direction. This article focuses on how to think about using both sides of the equity real estate investing coin, public and private, to maximize access and potentially improve the overall risk-adjusted return profile.

This article first appeared in the November 2024 edition of IREI Americas (subscription required).

Senior real estate credit specialists from LaSalle discuss the rising significance of senior real estate mortgage credit in investment portfolios with Institutional Real Estate Investor. They explore its ability to provide steady income and downside protection, the growing role of alternative lenders, and the current market opportunity. The article examines how this strategy offers attractive risk-adjusted returns, portfolio diversification, and enhanced resilience in today’s dynamic economic environment.

We regularly receive questions about past property market dislocations and what they might tell us about today, such as: Is office the new retail?, Will the 7+ years it took retail to rebalance be a template for office? and Should we be worried about the wave of supply in US apartments?

In our latest ISA Focus report, Rebalancing past and present, we engage in patten recognition across a range of historical episodes of occupier market challenges. We present a framework for how these imbalances tend to be resolved, and discuss the range of structural and cyclical factors that drive rebalancing. We also present a selection of historical case studies from around the world, highlighting the complex nature of the rebalancing process and how it can occur not only at different speeds, but also with “bumps in the road” for investors.

We conclude the report with a refresh of our ISA Focus: Revisiting the future of office, noting in particular that there will be specific investment opportunities that arise as the current rebalancing cycle plays out.

Important notice and disclaimer

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

As traditional lenders step back, the real estate debt market is opening up new avenues for institutional investors. In a recent Q&A with IREI, LaSalle’s Jen Wichmann, Senior Strategist and SVP of Research and Strategy, discusses the evolving landscape of real estate debt investments. From long-term trends and current market opportunities to the benefits of stable cash flow and downside protection, Wichmann provides insights into the sector.

Wichmann addresses several key topics relevant to investors considering real estate debt strategies:

The $1.5 trillion commercial real estate refinancing need in 2024-2025

How real estate debt offers downside protection and stable cash flows

Opportunities in the growing European alternative credit market

Expectations for real estate debt markets in late 2024 and early 2025

One of the most important factors we consider when deciding where to invest capital is the transparency of a real estate market. This encompasses the transparency of market fundamentals and investment performance, as well as:

its legal and regulatory transparency,

the prevalence of listed vehicles,

the transparency of transactions processes, and

the transparency of reporting on sustainability factors.

During times of heightened uncertainty, transparency is more important than ever as a foundation that allows real estate occupiers, investors and lenders to operate and make decisions with confidence.

Our latest ISA Focus report, Transparency and Strategy, explores these factors and their implications for real estate investors. We release this report alongside the Global Real Estate Transparency Index (GRETI) for 2024. GRETI is a joint publication between LaSalle and our parent company, JLL, which is based on a global survey of our extensive network of real estate market experts.

Important notice and disclaimer

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

Last year, we released the inaugural edition of LaSalle’s ISA Portfolio View, where we discussed the art and science of portfolio construction and why it matters most when market conditions change suddenly. That was certainly true at the time of last year’s release and remains so today.

In this year’s edition, we cover the five foundational concepts of portfolio management below, and how they should be considered alongside an investor’s objectives and values to devise a strategy for their portfolio.

Why real estate lays out the case for property exposure in a multi-asset context?

Why global considers the benefits of expanding horizons beyond an investor’s domestic market?

Why be sector smart tries to make sense of the recent changes in relative sector performance with an eye to building resilient portfolios?

Why be quadrant smart addresses the interplay among the “four quadrants” of real estate?

For 2024, we have also updated ISA Portfolio View to include the most recent available data, and added new sections on:

long-term real estate returns relative to stocks and bonds,

debt returns’ correlation to other assets, and

the effect of leverage on both risk and returns.

The speed and unpredictability of market changes over the last few years highlights the importance of not only planning ahead by thinking carefully about how to create real estate portfolios that can be expected to be resilient, but also working with an asset-class expert who understands the nuances presented by real estate.

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

This article first appeared in the Fall 2024 edition of NAREIM Dialogues.

LaSalle’s Julie Manning writes about our latest report with ULI that provides an industry-wide framework for commercial real estate to address how physical climate risk data can be used in decision-making and supporting investment performance.

Using data to evaluate physical climate risk

Measuring physical climate risk is of growing importance to institutional real estate managers and their investors, at both the individual property and portfolio levels. Of the $850 billion of commercial real estate assets tracked by NPI, LaSalle estimates $285 billion, or 34%, is situated in high and medium-high climate risk zones in the US.

Increasingly, being able to assess an asset’s risk exposure, and knowing how to price that risk into management strategies, are essential parts of operating a portfolio. While data is key to this assessment, understanding how to leverage the right data is even more important. With so much climate risk data available in the market, how can organizations manage and find data that gives them manageable, impactful and usable insights? And more importantly, what should managers do with these insights?

Real estate investors have a meaningful opportunity as the world transitions to a more decarbonized economy. In the video below, Sustainability experts from LaSalle, alongside JLL’s Global Head of Sustainability Services discuss this transition, and the actions that LaSalle is taking today.

Real estate investors have a meaningful opportunity as the world transitions to a more decarbonized economy. Energy-related performance and investment returns are becoming increasingly correlated, and we aim to stay ahead of the curve and capitalize on this long-term trend by decarbonizing the built environment as a means of delivering accretive outperformance.

This article first appeared in PropertyEU’s State of Logistics report

LaSalle’s Petra Blazkova recently joined Property EU’s State of Logistics 2024 conference in Amsterdam to present the firm’s inaugural Paths of Distribution Score research, which gives the ability to compare logistics locations at a micro, market, country and pan-European level.

LaSalle identifies top logistics locations in Europe

Paris and the surrounding Île-de-France region are the top micro-locations for efficient logistics distribution in Europe, according to a new study by LaSalle Investment Management.

The Paths of Distribution study considered over 150,000 micro-locations across the UK and EU, scoring them based on factors like manufacturing output, consumer spending, infrastructure, and labour costs. It also took into account the location of Amazon warehouses and analyzed data from REITs and other real estate databases.

Presenting the results at the Amsterdam logistics event, Petra Blazkova, Europe head of Core and Core-plus Research and Strategy, LaSalle Investment Management, pointed out that the data provides valuable insights for investors seeking the most efficient and attractive logistics locations with the greatest potential for long-term rental growth.

One of our key conviction sectors for real estate investment over the last few years has been logistics. It has been a particular focus of our research, as we seek to identify investment opportunities in prime locations. But with continued uncertainty around variables such as energy prices and supply chains being disrupted, cost uncertainty is high across the continent for logistics providers.

Location, however, is a key variable which distributors can still control, and so it is more important than ever: optimising your choice of location can help minimise exposure to these other risks and protect your supply chain.

LaSalle’s Paths of Distribution Score 2024

LaSalle’s inaugural “Paths of Distribution Score,” focuses on the geography of the European logistics market. This innovative, granular new research gives us the ability to compare logistics locations at a micro, market, country and pan-European level, with extensive flexibility for understanding, benchmarking and ranking locations – and opportunities to deploy capital – at both micro and macro scale. As investors in the sector, this new insight into the most resilient logistics markets in Europe informs our portfolio composition and asset management.

This article first appeared in the Summer 2024 edition of PREA Quarterly

LaSalle’s Global Head of Research and Strategy, Brian Klinksiek, discusses how ex-US investors are viewing the US real estate market.

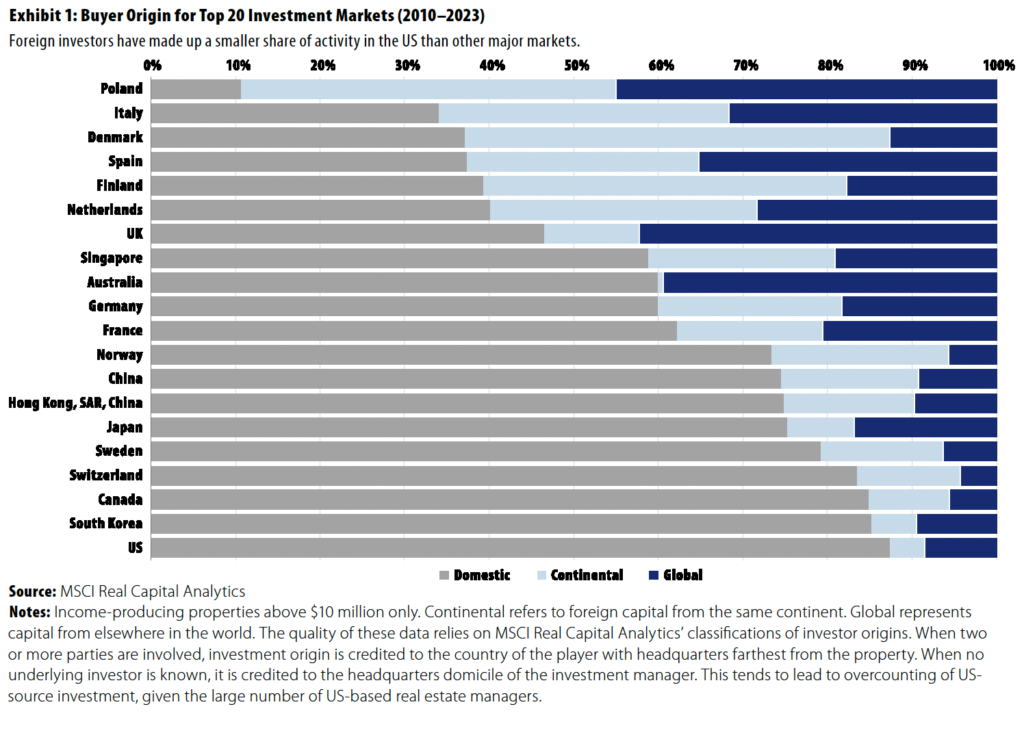

Foreign investors are an important—if far from dominant—source of capital for US commercial real estate. Since 2010, foreign investors have made up around 12% of total US investment activity, compared with the 30%–60% range for most other major developed markets, according to MSCI Real Capital Analytics (Exhibit 1). However, foreign investors also play a meaningful role as limited partners in funds. According to the PREA Investor Composition Survey, investors from outside the US in 2022 held nearly 18% of the NCREIF Fund Index—Open End Diversified Core Equity (NFI-ODCE) net asset value, a share that has risen steadily from less than 5% in 2012. Moreover, in some phases of the market, offshore capital has acted as the marginal buyer of certain types of real estate, giving an outsize impact on pricing.

Investors broaden their real estate holdings outside their home countries for many reasons, including to diversify, expand the opportunity set, and avoid crowded capital markets at home. The drive to expand globally is especially strong for investors in countries with excess savings in the form of well-funded defined benefit pension systems (e.g., Northern Europe), mandatory retirement savings programs (superannuation in Australia), or sovereign wealth funds (many energy exporters). LaSalle has long been an advocate of “going global”; while not the focus of this article, LaSalle covers the case for global investing in its ISA Portfolio View report.

While traditional banks’ appetite for providing commercial real estate loans has declined, other lenders (including investment management firms such as LaSalle) have moved in to fill the funding gap. As a result, we have recently seen increasing interest from institutional investors in real estate debt.

But what is it about real estate debt that makes it a compelling investment? As the second largest of the “four quadrants” of real estate, it has a value in the US and Europe alone of approximately US $4.5 trillion, representing an enormous opportunity. Real estate debt historically has produced competitive risk-adjusted returns in addition to showing low correlation to other assets.

In our latest research, we examine the three-part case for investment, including:

Real estate debt’s place in institutional portfolios,

The role of non-bank lending, and

The debt opportunity today, which takes advantage of a looming debt funding gap and attractive pricing.

Important notice and disclaimer

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

This article first appeared in the Spring 2024 edition of PREA Quarterly

LaSalle’s Global Head of Research and Strategy, Brian Klinksiek, discusses how the definition of core real estate is changing for investors, and what that could mean for their strategies.

A surprising standout as the most conversation-provoking exhibit from LaSalle’s ISA Outlook 2024 is titled “LaSalle’s Changing Definition of Core.” The simple table, reproduced for this article, contrasts a traditional core mind-set against an emerging “new” core mind-set. The former is focused on classic real estate metrics, such as credit quality and lease length, and flatters the property types that tend to score well against them, such as office. The latter is a more evidence-based approach focused on predictability and growth of actual cash flows, a lens that tends to favor the living sectors and niche property types and subtypes, such as medical office.

Taking a step back, the definition of core can be framed in various ways. It may be cast in relation to the other main “styles” of real estate investment—value-added and opportunistic—in that core is supposed to offer lower but safer and more predictable returns than either of those. Defining this with specificity might involve formal labels and thresholds, such as maximum leverage levels and property type characterizations. Assets and portfolios on the correct side of such definitions would be considered core and those beyond them would not be. Of course, financial theory suggests that the fundamental value of an asset should derive from the characteristics of its cash flows, not its conformance with metrics, criteria, and labels. Given that core portfolios are meant to deliver more reliable returns than non-core ones, an understanding of their sensitivity to factors such as economic growth and inflation and their vulnerability to operational challenges should be more important than how they align with some prescribed taxonomy. In this article, I take each of the classic metrics covered in the LaSalle chart and address why a change of mind-set may lead to better core portfolios.

This article first appeared in Winter 2024 edition of PREA Quarterly

LaSalle’s Global Head of Research and Strategy, Brian Klinksiek, discusses why it’s important to go beyond heuristics to find relative value in global real estate.

Which global real estate markets are ahead and which are behind in the process of repricing?

This question, along with its many variations, has been by some margin the most frequent one asked of me when presenting LaSalle’s recently released ISA Outlook 2024. Investors understandably want to know where they can find value amid real estate capital markets that continue to adjust to higher interest rates. They want to focus their efforts on geographies and sectors for which the bulk of the price adjustment is in the rearview mirror instead of still lying ahead.

Attempts to answer this question with numbers often begin with simple comparisons of peak-to-current value declines. The implicit logic is that larger-measured todate declines for a market indicate that it is farther along in the repricing process or, simply, that it is cheaper and thus attractive. But these sorts of analyses are plagued by a range of measurement and interpretation issues that complicate comparisons. At best, they can lead to contradictory conclusions; at worst, they may contribute to missteps in investment strategy. Some of the key challenges are explored below.

Petra Blazkova discusses our findings in LaSalle’s ECGI 2023 report.

Our latest LaSalle European Cities Growth Index (ECGI) ranks European cities with the strongest economic prospects based on data inputs of economic growth, human capital, business risk and – for the first time – extreme heat.

The 2023 edition highlights the steady strong positions of both London and Paris, which are set to account for more growth than Europe’s next nine top-ranked cities combined. Interestingly, Paris has overtaken London as the top destination for venture capital funding for the first time since LaSalle began tracking this data in 2006, receiving particularly elevated levels of investment into its technology sector.

Nordic cities appear to have an increasing advantage due to demographic trends, a skilled workforce and world-leading pharma, industrial tech and creative industries; they account for a quarter of the top 20 cities. German cities have continued to perform strongly in the index despite slow population growth. On the other hand, Rome and other Italian cities’ rankings are most negatively impacted after a new factor accounting for extreme heat days was added to the ECGI this year.

Elsewhere, Prague and Warsaw have been identified as having promising growth prospects as more expats return and high-skilled workers remain, with this “brain gain” leading them to their highest scores since the global financial crisis. The index also reflects that Warsaw is becoming an attractive place for employment in the technology sector and Prague is forecast to benefit from a jobs boom.

Brian Klinksiek, Global Head of Research and Strategy (L) and Eduardo Gorab, Head of Global Portfolio Research and Strategy, LaSalle Global Solutions (R), take a look at the why and how behind building diversified and resilient global real estate portfolios.

The art and science of portfolio construction matters most when market conditions change suddenly. This has never been truer than in the past few years, which saw major pivots in capital markets as policymakers shifted from trying to stimulate the economy at the start of the pandemic, to applying the breaks to prevent inflation running out of control. The speed and unpredictability of these changes highlights the importance of planning ahead by thinking carefully about how to create portfolios that can be expected to be resilient. Foundational concepts of portfolio management such as diversification and risk management should be considered alongside an investor’s objectives and values to devise a strategy for their portfolio.

It is with these factors in mind that we release first edition of LaSalle’s ISA Portfolio View, which seeks to answer five foundational questions about real estate:

Why real estate lays out the case for property exposure in a multi-asset context?

Why global considers the benefits of expanding horizons beyond an investor’s domestic market?

Why be sector smart tries to make sense of the recent changes in relative sector performance with an eye to building resilient portfolios?

Why be quadrant smart addresses the interplay among the “four quadrants” of real estate?

In many ways the ISA Portfolio View is the continuation of a longstanding strand of LaSalle’s analysis that would typically form the latter chapters of the Investment Strategy Annual. In this new standalone edition, we draw from a deep pool of experts from around the firm, acknowledging the interconnectedness of real estate opportunities: across borders, across sectors, and across quadrants. We welcome your questions and feedback.

Important Notice and Disclaimer

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

Brian Klinksiek’s article appears in Issue 12 of Summit, the official publication of AFIRE, the association for international real estate investors focused on commercial property in the United States.

Even as the US has exported trends that have transformed global property markets, several key trends originating in Europe are likely to shape property in the US and globally in the years ahead.

The opportunity to take ideas and best practices from one part of the world and implement them in another is, alongside diversification benefits, one of the great advantages of investing real estate capital across borders. Cyclical and secular themes tend to go global, albeit with leads and lags. Having a global perspective can give an investor an early-mover advantage over other players.

Historically, a common (but not exclusive) pattern has been for concepts to debut in US before emerging elsewhere. This was mirrored in my own career trajectory, which was shaped by the export of American business models. I moved from Chicago to London in 2009, and later to Hong Kong, to help my colleagues implement strategies in sectors that were established in the US but had been nascent elsewhere, such as multifamily apartments and self-storage. LaSalle has long tracked these differences in sector institutionalization and maturity on its “Going Mainstream” framework.

London ranks as Europe’s leading city for projected real-estate occupier demand for the sixth year running in the latest annual edition of the European Cities Growth Index (“ECGI”, formerly the European Regional Growth Index, or “E-REGI”). Following closely behind, Paris retains its position as one the “Big Two” European cities owing to its position as one of Europe’s key innovation and technology hubs.

While London retains its top position, its ECGI score worsened compared to last year, due to pressures on GDP growth. In 2022, the ECGI score worsened for 57 cities across Europe, the highest number since the Great Financial Crisis.

Polarization between London and UK regional cities also continued to widen in this year’s index.

Conversely, German cities proved to be less volatile in economic crisis and complementary of each other, with four German cities making it into the index’s top 20.

More broadly, since the ECGI’s inception in 2000, only London, Paris and Munich have consistently ranked in the top 10. Moreover, Amsterdam’s inclusion in the list this year comes due to the city’s human capital and employment growth prospects which remain exceptionally strong.

LaSalle Investment Management (“LaSalle”) announced that its flagship core institutional real estate fund, LaSalle Property Fund (“LPF” or “the fund”), bolstered its life sciences portfolio with a majority interest acquisition in 3215 Merryfield Row, a Class A+ life sciences building located in the heart of the high-barrier-to-entry market of Torrey Pines in San Diego, California. LPF acquired its stake in 3215 Merryfield Row through a joint venture with a publicly traded REIT.

The investment aligns with the fund’s strategy of investing in best-in-class life sciences properties in high-conviction markets as part of its national, diversified portfolio. With the addition of a stake in 3215 Merryfield Row, life sciences and medical office properties now comprise 13 percent of LPF’s portfolio. LPF’s life science investment includes Illumina’s world headquarters, located in the UTC submarket of San Diego, in which it acquired a partial interest in 2019.

Jim Garvey, President of LaSalle Property Fund, said: “We have high conviction in the life sciences sector given the strong tenant demand, which is a function of the continuing advancement in pharmaceuticals, medical devices and therapeutics. 3215 Merryfield Row is an exceptional property, both in its location, and best-in-class construction, and comes with the added bonus of a leading partner who we know and trust. We’re very pleased to add 3215 Merryfield Row to LPF’s portfolio.”

Erick Paulson, LaSalle Acquisitions Officer, added: “This is a special property with a premier location, a strong credit tenant, and an outstanding operating partner for LPF. Life sciences properties continue to be in high demand due to their challenging and often expensive construction and should provide excellent cash flow and appreciation for well capitalized buyers looking to achieve long-term gains.”

Constructed in 2018 with state-of-the-art life science specs, the property is fully leased to Vertex, a global biotech company focused on small molecule therapeutics and cystic fibrosis, and serves as one of the company’s three global research hubs. Largely considered one of the most architecturally significant life science properties on the West Coast, 3215 Merryfield Row is LEED Gold Certified and includes glass interior walls, a 1,500-square-foot Learning Lab for STEM education programs, an interactive art display in the lobby, and an air circulation system that is designed to bring in 100 percent outside air.

The property also benefits from its coveted location in the sought-after Torrey Pines submarket, which has a life sciences vacancy rate of just 0.3 percent. More broadly, LaSalle Research & Strategy pegs San Diego as the nation’s third-best life sciences market. San Diego is home to more than 1,300 life science companies and is comprised of 19.8 million square feet of life science space supported by strong fundamentals, including a record low direct vacancy rate of 2.3 percent and an average triple-net asking rate that has risen 166 percent since 2015.

About LaSalle Investment Management

LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, we manage approximately $82 billion of assets in private equity, debt and public real estate investments as of Q2 2022. The firm sponsors a complete range of investment vehicles including open- and closed-end funds, separate accounts and indirect investments. Our diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. For more information please visit www.lasalle.com and LinkedIn.

NOTE: This information discussed above is based on the market analysis and expectations of LaSalle and should not be relied upon by the reader as research or investment advice regarding LaSalle funds or any issuer or security in particular. The information presented herein is for illustrative and educational purposes and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy in any jurisdiction where prohibited by law or where contrary to local law or regulation. Any such offer to invest, if made, will only be made to certain qualified investors by means of a private placement memorandum or applicable offering document and in accordance with applicable laws and regulations. Past performance is not indicative of future results, nor should any statements herein be construed as a prediction or guarantee of future results.

Company news

Jun 18, 2025 LaSalle acquires Ruby Stella Hotel in Clerkenwell

The five-building industrial complex was acquired on behalf of the LaSalle Property Fund.

Feb 11, 2025 Kunihiko Okumura and Steve Hyung Kim appointed Asia Pacific leaders

Keith Fujii to assume the role of Chairman of Asia Pacific, with all changes to be effective July 1, 2025.

Make sure you’ve spelled everything correctly, or try searching for something else. If you still can’t find what you’re looking for, you can always Contact us to talk to someone.

JLL Income Property Trust, an institutionally managed daily NAV REIT (NASDAQ: ZIPTAX; ZIPTMX; ZIPIAX; ZIPIMX) with approximately $6.7 billion in portfolio assets and advised by LaSalle Investment Management, announced today the acquisition of Patterson Place a 25,000-square-foot retail center in Durham, North Carolina. The retail property is anchored by Duke Medical Plaza, which was recently acquired by JLL Income Property Trust. Patterson Place was acquired for approximately $14.5 million.

“Patterson Place is a well-located, medical office-anchored retail center that we believe benefits from strong foot traffic generated by the recently acquired Duke Medical Plaza along with a strong tenant roster and a prime location at the intersection of two major thoroughfares that connect dense population centers,” said JLL Income Property Trust President and CEO Allan Swaringen. “We have conviction in the Raleigh market and believe the outlook for retail with a strong anchor tenant looks positive as pandemic restrictions ease and consumer spending remains elevated. All of these factors point to a strong investment that should yield long term, stable cashflow for our stockholders.”

Constructed in phases between 2010 and 2015, Patterson Place tenants include national retailers such as Five Guys, AT&T and Moe’s. The weighted average lease term is greater than five years. In addition to its strong tenant roster, Patterson Place benefits from local demographic tailwinds. According to LaSalle Research & Strategy, Raleigh’s in-migrations is expected to outpace the US rate with a high-concentration of prime-age workers over the next 10 years. Within a one-mile radius of the property annual population growth is projected to grow twice as fast as the US average, which should drive continued consumer demand.

The property’s location just off of Interstate 40 puts it at the center of a key regional connector between Durham, Research Triangle Park and Raleigh and makes it accessible to Duke University and University of North Carolina, both of which are just a 10-minute drive.

JLL Income Property Trust’s retail allocation is 14 properties in 13 key markets valued at $789 million and representing approximately 13 percent of its overall portfolio.

JLL Income Property Trust is an institutionally managed, daily NAV REIT that brings to investors a growing portfolio of commercial real estate investments selected by an institutional investment management team and sponsored by one of the world’s leading real estate services firms.

About LaSalle Investment Management LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, we manage approximately $82 billion of assets in private equity, debt and public real estate investments as of Q2 2022. The firm sponsors a complete range of investment vehicles including open- and closed-end funds, separate accounts and indirect investments. Our diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. For more information please visit www.lasalle.com and LinkedIn.

NOTE: This information discussed above is based on the market analysis and expectations of LaSalle and should not be relied upon by the reader as research or investment advice regarding LaSalle funds or any issuer or security in particular. The information presented herein is for illustrative and educational purposes and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy in any jurisdiction where prohibited by law or where contrary to local law or regulation. Any such offer to invest, if made, will only be made to certain qualified investors by means of a private placement memorandum or applicable offering document and in accordance with applicable laws and regulations. Past performance is not indicative of future results, nor should any statements herein be construed as a prediction or guarantee of future results.

Company news

Jun 18, 2025 LaSalle acquires Ruby Stella Hotel in Clerkenwell

The five-building industrial complex was acquired on behalf of the LaSalle Property Fund.

Feb 11, 2025 Kunihiko Okumura and Steve Hyung Kim appointed Asia Pacific leaders

Keith Fujii to assume the role of Chairman of Asia Pacific, with all changes to be effective July 1, 2025.

Make sure you’ve spelled everything correctly, or try searching for something else. If you still can’t find what you’re looking for, you can always Contact us to talk to someone.

More economic and geopolitical history unfolded in the first half of 2022 than typically occurs during the span of several “normal” years. The quaint concept of “normality” may itself prove to be an artifact of history. Yet, the mid-year ISA describes how real estate held up well despite all the tumult. Strategies we set out in 2021, performed as expected, or sometimes even better than expected. Strategy shifts recommended by LaSalle for the second half of the year are modest, despite a renewed focus on the changing macro environment.

Real estate generally provided shelter during the waves of volatility that swept through the securities markets in the first half of the year. In the second half, we foresee different dynamics unfolding as described in Chapter 1, and in the specific strategy shifts recommended in Chapter 2. The big change has been the end of ultra-low interest rates in Western countries. Finally, we revisit the role of real estate in a portfolio in Chapter 3, based on new research done with JLL for the bi-annual Transparency Index, as well as the most recent updates to the correlations with other asset classes.

The most important change in the macroeconomic outlook has been the regime shift from highly accommodative to tightening monetary policies by Western central banks. Many world events simultaneously contributed to this inflection point including: the re-opening of economies after COVID-19, Russia’s invasion of Ukraine, trade wars, and government stimulus spending. Although these pressures were building in 2021, there is no escaping the fact that the financial and commodity markets shifted sharply in the first half of 2022.

In this mid-year update, we focus on the ways that assets and portfolios can be positioned to weather a sustained period of high inflation. We acknowledge that each country is in a slightly different position in the transition from low to higher inflation and that each central bank will react differently to the mix of cost-push and demand-pull inflationary forces.

Other highlighted trends include the continuing competition and complementarity between virtual and physical space. Patterns that affect both asset and sector selection are now coming more clearly into view. Also, we point to the continued momentum of the sustainability revolution as investment managers commit to reducing the carbon footprint of their portfolios, while also grappling with climate risk forecast challenges, transition risks from new regulations, and social issues like housing affordability or health and well-being factors that affect tenants.

Thanks for your submission. This report has been expertly crafted with insights

gleaned from the knowledge and expertise provided by LaSalle Investment Management’s

research team.

LaSalle Investment Management (“LaSalle”) will develop Munich’s first hybrid timber office building, in collaboration with ACCUMULATA Real Estate Group (“ACCUMULATA”). The building is being constructed on behalf of Encore+, LaSalle’s flagship pan-European fund.

Situated on Elsenheimerstrasse in the city’s Westend district, the office building will have a floor area of approximately 16,000 m2. With dismantling of the existing building on site already underway and construction due to begin in the third quarter of this year, the project is scheduled for completion during the first quarter of 2024. Lettings are already being marketed in collaboration with CBRE, the lead estate agent.

Designed by the leading Munich-based architectural firm Oliv Architekten, the asset will provide flexible, multifunctional spaces including a ground-floor café/bistro and landscaped roof terrace, as well as various wellness amenities, including a yoga studio and a relaxation lounge. Tenants will also enjoy bicycle parking, electric charging points and a smart underground car parking facility. Furthermore, the building will provide customisable office units and creative collaboration spaces, ensuring the asset is well positioned for the future.

In terms of its environmental credentials, the project meets the highest sustainability standards across all areas, including construction, materials and operations. Having already received a DGNB “Platinum” precertification, the asset will be constructed using concrete reclaimed from the existing building currently situated at this location. All materials used in construction will be documented in a material passport, showing where and how the various components were sourced and installed, ensuring they can be repurposed at the end of their service life. These measures are projected to reduce embodied carbon by up to 25%.

Embodied carbon will be low at 366kg CO2e/sqm, significantly below the RICS Building Carbon Database (offices) average benchmark of 1291kg CO2e/sqm.

The use of timber in the building’s load-bearing structure will ensure that approximately 1,100 tonnes of carbon will remain stored in the building fabric, rather than emitted into the atmosphere. During the course of the asset’s lifespan, emissions associated with the building’s operation will be reduced by 65% in comparison to a typical office building through the integration of a photovoltaic system, efficient heating, cooling and ventilation systems and the use of a ground water heat pump. The building will also harvest and store rainwater, supplying irrigation systems for the benefit of surrounding green areas.

David Ironside, Fund Manager of Encore+ at LaSalle Investment Management, commented: “This is an industry-leading and best-in-class project. The first of its kind in Munich, its design in accordance with circular economy principles and resource-conserving operation will serve as a benchmark in sustainable real estate. Located in one of the most sought-after office submarkets in Munich, the property will be extremely well placed to meet the ever-evolving demands of future tenants around sustainability, quality, amenities and infrastructure, while providing attractive long-term returns for our investors.”

Markus Diegelmann, Managing Partner at ACCUMULATA Real Estate Group, added: “The start of demolition marks an exciting first step in the development of what will be one of the most sustainable office projects in Munich. At ACCUMULATA, we aim to promote the concepts of urban mining and the circular economy within the construction sector and this project is firmly aligned with this objective. By utilising ultra-high-quality and recyclable materials, we are creating an office building that can meet occupiers’ shifting requirements, both in terms of flexible working environments and sustainability standards.”

Georg Illichmann, Managing Director at CBRE GmbH, said: “As the first hybrid timber office building to be constructed in Munich, the project achieves all the modern-day requirements tenants demand from office buildings: easy accessibility to public transport, sustainability credentials and working spaces that promote communication, creativity and innovation. The building’s use of timber, unique to the Munich office market, will not only support the building’s sustainability credentials but also the wellbeing of occupiers. At CBRE, we are proud to be leading on the marketing of this unique asset and be involved in ground-breaking project in the German real estate market as the lead estate agent.”

About LaSalle Investment Management LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, we manage approximately $82 billion of assets in private equity, debt and public real estate investments as of Q2 2022. The firm sponsors a complete range of investment vehicles including open- and closed-end funds, separate accounts and indirect investments. Our diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. For more information please visit www.lasalle.com and LinkedIn.

NOTE: This information discussed above is based on the market analysis and expectations of LaSalle and should not be relied upon by the reader as research or investment advice regarding LaSalle funds or any issuer or security in particular. The information presented herein is for illustrative and educational purposes and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy in any jurisdiction where prohibited by law or where contrary to local law or regulation. Any such offer to invest, if made, will only be made to certain qualified investors by means of a private placement memorandum or applicable offering document and in accordance with applicable laws and regulations. Past performance is not indicative of future results, nor should any statements herein be construed as a prediction or guarantee of future results.

Company news

Jun 18, 2025 LaSalle acquires Ruby Stella Hotel in Clerkenwell

The five-building industrial complex was acquired on behalf of the LaSalle Property Fund.

Feb 11, 2025 Kunihiko Okumura and Steve Hyung Kim appointed Asia Pacific leaders

Keith Fujii to assume the role of Chairman of Asia Pacific, with all changes to be effective July 1, 2025.

Make sure you’ve spelled everything correctly, or try searching for something else. If you still can’t find what you’re looking for, you can always Contact us to talk to someone.

LaSalle Investment Management (“LaSalle”) has completed the acquisition of a prime new-build residential asset in Frederiksberg (Copenhagen), on behalf of its open-ended pan-European LaSalle E-REGI fund.

The transaction represents LaSalle E-REGI‘s first investment in a residential property in Copenhagen, exemplifying the Fund‘s appetite for best-in-class residential assets in Europe’s key cities. It follows the recent acquisition of ‘Lacus Quartier’ in Berlin, which provided a strategic foundation for further growth in the residential sector for the Fund. Copenhagen, underpinned by its strong fundamentals and buoyant growth forecast for disposable income, was ranked as the eighth strongest city in LaSalle’s 2021 European Cities Growth Index and is earmarked as a key market for LaSalle.

The property is located on H.C. Ørsteds Vej in a vibrant residential area of Frederiksberg, in central Copenhagen. The location provides excellent public transport access with a bus stop directly in front of the property and a metro station less than five minutes’ walk. It benefits from close amenities, such as Frederiksberg High Street, as well as the pedestrianised District of Copenhagen and recreational and green areas such as The Lakes and the “Assistens Cemetery” park. Additionally, the Forum, which hosts many concerts and art exhibitions, as well as both Copenhagen University and Copenhagen Business School are located nearby.

Built in 2019, the asset currently operates with very low carbon emissions and boasts an exceptional energy efficiency rating, which is supported by rooftop solar panelling. The building comprises over 3,800m² with 24 high-quality residential apartments which range from one to six rooms and a ground-floor commercial unit which is currently let to leading Danish grocery store chain Netto. The property also holds 40 parking spaces.

Uwe Rempis, Managing Director and Fund Manager of LaSalle E-REGI, commented: “This acquisition marks a key milestone in the Fund’s strategy to further diversify its country and asset allocation by adding its first Danish residential property. The asset’s location, combined with its strong sustainability credentials and the robust demand for residential space in central Copenhagen, is projected to drive strong long-term rental income.”

Jérôme Hamelin, Head of Transactions Western Continental Europe at LaSalle, added: “The asset is characterised by its strong fundamentals in a central urban location with excellent connectivity and amenities. In addition to being a high quality, resilient asset in a highly sought-after residential area, it also supports the Fund’s sustainability strategy with its state-of-the-art energy efficiency characteristics.”

LaSalle was advised on the transaction by Keystone Investment Management, who will assist in managing the asset, Accura (Legal), X-Project (Technical) and KPMG (Tax). EDC advised the vendor on the sell-side.

About LaSalle Investment Management LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, we manage approximately $82 billion of assets in private equity, debt and public real estate investments as of Q2 2022. The firm sponsors a complete range of investment vehicles including open- and closed-end funds, separate accounts and indirect investments. Our diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. For more information please visit www.lasalle.com and LinkedIn.

NOTE: This information discussed above is based on the market analysis and expectations of LaSalle and should not be relied upon by the reader as research or investment advice regarding LaSalle funds or any issuer or security in particular. The information presented herein is for illustrative and educational purposes and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy in any jurisdiction where prohibited by law or where contrary to local law or regulation. Any such offer to invest, if made, will only be made to certain qualified investors by means of a private placement memorandum or applicable offering document and in accordance with applicable laws and regulations. Past performance is not indicative of future results, nor should any statements herein be construed as a prediction or guarantee of future results.

Company news

Jun 18, 2025 LaSalle acquires Ruby Stella Hotel in Clerkenwell

The five-building industrial complex was acquired on behalf of the LaSalle Property Fund.

Feb 11, 2025 Kunihiko Okumura and Steve Hyung Kim appointed Asia Pacific leaders

Keith Fujii to assume the role of Chairman of Asia Pacific, with all changes to be effective July 1, 2025.

Make sure you’ve spelled everything correctly, or try searching for something else. If you still can’t find what you’re looking for, you can always Contact us to talk to someone.

LaSalle Investment Management (“LaSalle”) announced its flagship core real estate fund in Canada, LaSalle Canada Property Fund (“LCPF” or “the fund”), expanded its portfolio through a joint venture acquisition of 21 mid-bay industrial properties in the Greater Toronto Area (“GTA”) in partnership with an international capital source. The properties total nearly 810,000 square feet and are strategically located in the Mississauga industrial node, the premier submarket for servicing Canada’s largest city and just a short drive to Pearson International Airport. LCPF is participating in the acquisition through its value-add sleeve.

The acquisition represents a compelling value-add opportunity for both partners with near-term upside given rents are 60 percent below market rate and the weighted average lease term is just 1.5 years. Toronto is North America’s third largest industrial market and is land constrained due to protective zoning in the surrounding “Greenbelt” area. Historically, these factors have created strong tenant demand for industrial property, driving vacancy for industrial product in the GTA to 0.9 percent, the lowest of any North American market.

John McKinlay, CEO of LaSalle Canada, said: “We’re thrilled to execute this transaction with our international partner, which helps both parties achieve our goal of increasing our exposure to well-located assets in the industrial sector. We feel our track record of successfully executing on all types of industrial investments, whether they are core, value-add or development, positions us well to create value and generate returns even in a hyper-competitive market such as Toronto.”

Mike Cornelissen, LaSalle Senior Vice President of Acquisitions, added: “This portfolio aligns with all of our preferred attributes in terms of mid-bay product type, location, scale and upside. It’s rare to find such well-located, quality industrial properties in the Greater Toronto Area, and we’re excited about the rental upside given the portfolio’s short weighted average lease term. We appreciate the efficient transaction process with our partners, and believe the assets will meaningfully enhance our portfolios.”

The portfolio is 98 percent leased, with buildings ranging from 18,000-81,000 square feet. The properties are designed to accommodate a wide range of tenant uses, including standalone buildings for single tenants.

The GTA stands out as one of North America’s top industrial markets, driven by high population growth through immigration and exceptional rent growth. This population growth should continue to drive e-commerce demand which relies on well-located mid-bay industrial product. Through the last three years, GTA’s industrial market rents have experienced a compound annual growth rate of 20 percent, meaningfully outpacing the 8-12 percent growth seen in top US markets over that same period.

About LaSalle in Canada

On an aggregate basis, LaSalle has executed more than C$7 billion in Canadian real estate since 2000, providing it with an in-depth understanding of the market. The formation of LCPF expanded LaSalle’s existing Canadian real estate product suite and investment vehicles, which include a series of closed-end commingled funds as well as separate accounts.

About LaSalle Canada Property Fund (LCPF)

LCPF is an open-ended fund targeting core properties in major markets across Canada. The fund is targeting commitments from Canadian and global institutional investors seeking access to the Canadian real estate market through a diversified, income-oriented vehicle. Launched in 2017, the fund aims to provide investors with immediate exposure to a diverse and mature portfolio comprised of office, industrial, mixed-use, retail and multifamily assets. Through its near-term pipeline of potential future investments, the fund will seek to take advantage of mispriced assets as it continues to grow.

About LaSalle Investment Management

LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, we manage approximately $82 billion of assets in private equity, debt and public real estate investments as of Q2 2022. The firm sponsors a complete range of investment vehicles including open- and closed-end funds, separate accounts and indirect investments. Our diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. For more information please visit www.lasalle.com and LinkedIn.

NOTE: This information discussed above is based on the market analysis and expectations of LaSalle and should not be relied upon by the reader as research or investment advice regarding LaSalle funds or any issuer or security in particular. The information presented herein is for illustrative and educational purposes and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy in any jurisdiction where prohibited by law or where contrary to local law or regulation. Any such offer to invest, if made, will only be made to certain qualified investors by means of a private placement memorandum or applicable offering document and in accordance with applicable laws and regulations. Past performance is not indicative of future results, nor should any statements herein be construed as a prediction or guarantee of future results.

Company news

Jun 18, 2025 LaSalle acquires Ruby Stella Hotel in Clerkenwell

The five-building industrial complex was acquired on behalf of the LaSalle Property Fund.

Feb 11, 2025 Kunihiko Okumura and Steve Hyung Kim appointed Asia Pacific leaders

Keith Fujii to assume the role of Chairman of Asia Pacific, with all changes to be effective July 1, 2025.

Make sure you’ve spelled everything correctly, or try searching for something else. If you still can’t find what you’re looking for, you can always Contact us to talk to someone.

LaSalle Investment Management (“LaSalle”) has completed the acquisition of ‘Lacus Quartier’ in Berlin on behalf of the pan-European LaSalle E-REGI fund.

LaSalle signed to acquire the new development from BUWOG in December 2020. The scheme opened its doors to residents for the first time in May 2021 and, following its first 12 months in operation, it has now achieved a 94% occupancy rate, demonstrating the strength of the asset’s offer and location to residents seeking high-quality rental homes in Berlin’s Weißensee district.

The scheme includes 230 high-quality apartments, between 35 and 113 m2 in size, and 88 of the units have a balcony or terrace. Car parking spaces and several e-charging stations are located in the building’s underground garage, and bicycle parking is available outdoors. The courtyard offers a plethora of leisure facilities for families such as a playground, table tennis and a racetrack for children. The property is managed by MVGM.

The neighbourhood is located in the up-and-coming district of Berlin-Weißensee between Gäblerstrasse, Gustav-Adolf-Strasse and Schmohlstrasse within Pankow, the capital’s most populous district. Weißensee benefits from a quiet and family-friendly environment, good public transport links and close proximity to the popular and steadily growing district of Prenzlauer Berg. A population increase of more than 10%[1] is expected for the entire Berlin-Pankow district by 2030.

Uwe Rempis, Managing Director and Fund Manager of LaSalle E-REGI, commented: “This acquisition marks a significant milestone for LaSalle E‑REGI, providing a strategic foundation to further growth in the residential sector for the Fund. We continue to deliver on our strategy to diversify the Fund’s sector allocation with best-in-class assets, prioritising the strongest cities across Europe, which will provide long-term stable income for our investors.”

Antonia Muelsch, Head of Transactions, Germany, at LaSalle, added: “As evidenced by Lacus Quartier’s high occupancy rate in such a short space of time, this market is experiencing strong demand of high-quality rental homes. With its diverse mix of one- to four-bedroom apartments, sophisticated amenities and excellent location, Lacus Quartier is attractive to a wide variety of resident demographics such as families, singles and older residents, and is set to provide secured and sustainable income for the Fund into the future.”

LaSalle was advised by Mayer Brown LLP (Legal), Witte Projektmanagement (Technical), KPMG (Tax) and CBRE (Buy-Side-Advice). Luther LLP (Legal) and BNP Paribas Real Estate GmbH (Transaction Broker) acted for the seller.

[1] Source: StatisticsDepartment Berlin-Brandenburg 2013/2019 / Report on population forecast for Berlin and the districts 2018 –2030

About LaSalle Investment Management

LaSalle Investment Management is one of the world’s leading real estate investment managers. On a global basis, we manage approximately $82 billion of assets in private equity, debt and public real estate investments as of Q2 2022. The firm sponsors a complete range of investment vehicles including open- and closed-end funds, separate accounts and indirect investments. Our diverse client base includes public and private pension funds, insurance companies, governments, corporations, endowments and private individuals from across the globe. For more information please visit www.lasalle.com and LinkedIn.

NOTE: This information discussed above is based on the market analysis and expectations of LaSalle and should not be relied upon by the reader as research or investment advice regarding LaSalle funds or any issuer or security in particular. The information presented herein is for illustrative and educational purposes and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy in any jurisdiction where prohibited by law or where contrary to local law or regulation. Any such offer to invest, if made, will only be made to certain qualified investors by means of a private placement memorandum or applicable offering document and in accordance with applicable laws and regulations. Past performance is not indicative of future results, nor should any statements herein be construed as a prediction or guarantee of future results.

Company news

Jun 18, 2025 LaSalle acquires Ruby Stella Hotel in Clerkenwell

The five-building industrial complex was acquired on behalf of the LaSalle Property Fund.

Feb 11, 2025 Kunihiko Okumura and Steve Hyung Kim appointed Asia Pacific leaders

Keith Fujii to assume the role of Chairman of Asia Pacific, with all changes to be effective July 1, 2025.

Make sure you’ve spelled everything correctly, or try searching for something else. If you still can’t find what you’re looking for, you can always Contact us to talk to someone.

The pandemic gave us time to reconsider our lives, our work, our relationships with families, friends, neighbors, and co-workers. It also fundamentally changed how we interact with technology and with our surroundings – in both the natural and built environments. For real estate investors, the pandemic rocked the foundation of the asset class. Yet, as our Mid-Year Update reveals, real estate has generally survived intact, and many markets are thriving in novel ways. Finally, the pandemic raised awareness for the possibilities for creating societal benefits through investment in low-carbon assets and in healthy, diverse communities.