-

Brian Klinksiek and Eduardo Gorab (L-R) discuss how the investment landscape as we reach the halfway point of 2024. “You take the blue pill—the story ends, you wake up in your bed and believe whatever you want to believe. You take the red pill… all I’m offering is the truth.”

– Morpheus to Neo, The Matrix (1999)

We published the global chapter of the ISA Outlook 2024 on November 14, 2023, just before euphoria about a potential ‘V’-shaped property market turnaround emerged. Interest rates fell quickly as financial markets priced in several US Federal Reserve (Fed) rate cuts in 2024. For a time, it looked as though our prediction that it would take a little longer for markets to digest a renewed spike in rates would not age well.

In this Mid-Year Update, however, we look back to find an outlook with an uncanny resemblance to that of six months ago. This is not because nothing has changed, but because the mood has gone full circle. The landscape remains characterized by interest rate volatility, soft fundamentals in some markets, and gaping quality divides, but also by pockets of considerable strength. Another factor that has not changed is that financial conditions (i.e., interest rates) remain the dominant driver of the market, and that political and geopolitical uncertainties are in focus in many countries (see LaSalle Macro Quarterly, or LMQ, pages 4-6).1

In this report, we discuss five themes we see driving real estate markets for the rest of 2024 and beyond. At our European Investor Summit in May, our colleague Dan Mahoney argued that—like Neo in the Matrix—we should take the red pill and endeavor to see the market as it is, not as we’d like it to be. Taking the red pill requires a realistic view on property values. It reveals as unlikely a return to an environment of ultra-low interest rates or uniformly benign fundamentals in the “winning” sectors.

But it does not mean that there will not be attractive investment opportunities. Unlike the bleak dystopia of The Matrix, there are many reasons for optimism, as well as signs that the coming months will come to be seen as a favorable investment vintage. That said, investing successfully will require a balance of big-picture perspective and granular discernment, and a mix of patience and willingness to take risk.

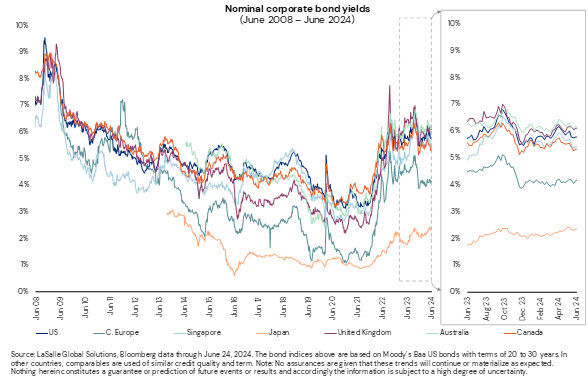

Interest rates – Still no map to the trail

Over the past year, we likened the interest rate path in most markets to a strenuous mountain trek: the relentless climb (2022), the range-bound altitude of an alpine ridge line (H1 2023), the unexpected upward turn in the trail (Q3 2023), and the mountain meadow of cooling inflation and expected rate cuts (Q1 2024). More recently, there have been upward turns in the interest rates trail whenever there have been signs of sticky inflation in the US and other key countries.

One thing is for sure: No map exists for this trail. While interest rates have big consequences for real estate capital markets, they are extremely difficult to predict. We continue to caution investors against overconfidence in their ability to forecast the path of long-term interest rates.

Mercifully, falling rates are not a necessary condition for a robust recovery in real estate transaction activity. Despite interest rates remaining elevated, property markets are already showing signs of finding their footing, such as renewed US CMBS issuance and resilient deal volumes in many markets and sectors.2 A key reason for this is that wherever interest rates have spiked over the past two and half years, especially Europe and North America,3 real estate prices have by now adjusted downward significantly. The relativities between expected returns for real estate and those for other asset classes now look more appropriate than they have in many months; in other words, more of the market is at or near fair value.4

That said, while lower rates are not necessary for real estate capital market normalization, greater stability in rates than we have been seeing would no doubt help. Interest rate volatility is the enemy of a smoothly functioning private real estate transaction market. Excessive movement in borrowing costs during due diligence periods can lead to dropped deals and re-trades. Moreover, when rates are volatile, the conclusions of fair value models are also volatile, impacting both buyers’ and sellers’ assessments of appropriate pricing. Looking at recent trends in the MOVE index,5,6 interest rate volatility appears to be gradually easing but is still elevated relative to recent history (see LMQ page 13).

Increasing stability in rates is welcome, but for now it is reasonable to expect continued strains in real estate capital markets that create both challenges and opportunities. Such conditions can represent favorable entry points for debt investors (lenders), distressed equity players and core investors seeking entry points below replacement

Macro – Deciphering divergence

Over the past half-year, interest rates have been increasingly influenced by widening divergences between near-term growth, inflation and monetary and fiscal policy outlooks. Most notably, the bond yield gap between the US and other markets, especially the eurozone, has widened. US growth and inflation have surprised on the upside, in the face of softening or stability elsewhere. Markets currently expect only one Fed rate cut in 2024, down from up to four earlier in the year.7 Meanwhile, in early June the Bank of Canada became the first G7 central bank to cut rates since the great tightening cycle began, with the European Central Bank (ECB) following shortly after (see LMQ page 7).

Regional groupings can obscure divergences within them. The key driver of eurozone softness is Germany (see LMQ page 23), owing to its reliance on manufacturing exports and past dependance on Russian energy. Meanwhile, the Spanish economy remains strong due to healthy consumption and tourism. Within North America, Canada’s economy is underperforming the US because the structure of its residential mortgage market makes it more exposed to higher rates.8 These intra-regional variations may have a range of impacts on property markets, for example by shifting the relative short-term prospects for demand and value.

Japan and China represent long-standing divergences that persist.9 In China, a loosening bias remains in effect as inflation hovers at around 0%.10 In Japan, monetary policy is gradually normalizing, but so far without triggering a big increase in interest rates (at least compared to elsewhere). In March, the Bank of Japan (BOJ) abandoned negative interest rates and ended most unorthodox monetary policies, though it has since held policy interest rates at around zero. Japan’s economy becoming more “normal” is generally a positive, but interest rate differentials have pushed the yen to a 34-year low against the US dollar (see LMQ page 14), creating upside risks to inflation.11 But notably, Japan remains the one major global market in which real estate leverage remains broadly accretive to going-in yields.

Aside from reinforcing the potential benefits of diversification, what do these divergences mean for investors? Mechanically, any unexpected relative softening of interest rates should, all else equal, be beneficial for relative value assessments of real estate in that market. But firmer rates in the US have predictably come alongside a stronger US dollar. This points to practical limits to global monetary policy divergences; central bankers are keenly aware that weaker currencies come with inflationary risks. Moreover, it is worth asking how persistent macro divergences will be; current divergences are rooted in timing differences of expected rate cuts, rather than an anticipated permanent disconnect.

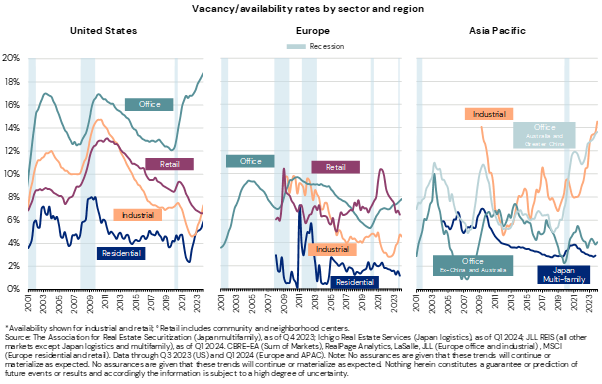

Renewed cyclicality — Ride the (supply) wave

For several years, secular themes and structural shocks have dominated the trajectories of global property markets. But there is a clear cyclical pattern reemerging in the form of a pronounced upswing in vacancy across global logistics markets, and in US apartments. The return of cyclicality in those favored sectors is having significant impacts on their near-term prospects.

The softening trend is not new. In the ISA Outlook 2024, we identified hot sectors “coming off the boil.” Part of this was down to normalizing demand levels, but elevated new supply was also a key driver. As expected, the softening we observed has continued to deepen, leading to outright rent declines in certain markets, especially for apartments in US sunbelt metros.

Softening fundamentals are not to be ignored, but we recommend investors to have the conviction to “ride the wave” of excess supply. Wide variation in supply levels at the market and submarket level means that investors with granular market data and the discipline to incorporate it into their market targeting processes should be positioned to select the most attractive markets and submarkets.

Moreover, the forces that create cycles sow the seeds of their own reversal; we expect the current supply wave to moderate soon, as evidenced by sharply falling construction starts (see LMQ page 25). Many of the projects being completed today broke ground when credible exit cap rate assumptions were several hundred basis points lower than today. Higher interest rates upended development economics; far fewer new developments can now be justified on today’s mix of land prices, construction costs and financial conditions.

Finally, investors should be prepared to think about cash flows in both real and nominal terms. When cooling nominal rental growth comes alongside cooling inflation, as it does today, it is possible for that to be consistent with solid real rental growth, depending on the relative magnitude of each.

The next chapters in secular change

Beyond the reassertion of supply cycles in some markets, there is an evolving mix of secular stories that deserve attention. Some of these are so long-standing that they could almost be considered constants. These include structural shortages of housing in most of Europe, Canada and Australia, as well as the widespread changing definition of core real estate in favor of more operational niche sectors and sub-types.12 We continue to be strong advocates for investment in undersupplied living sectors, and for participating in the institutionalization and growth of niche sub-sectors such as single-family rental (SFR) and industrial outdoor storage (IOS).

More dynamic themes that deserve a closer look include the stabilization of retail real estate and divergent office investment prospects:

- Rebalanced retail — In much of the world, the various sub-sectors of retail are on firmer ground than they have been in years. This owes to a nearly decade-long process of rebalancing, supported by normalizing post-pandemic demand trends and the removal, through demolition or irrelevance, of uncompetitive retail inventory. We have found retail assets to be some of the most stable performers in our portfolio in recent quarters. While the consumer mood is bifurcated between healthy higher-end households and lower-income households struggling with inflation’s hit to real spending power, physical retail has proven its enduring role in serving both convenience and experiential shopping. We are constructive on selective investment in several retail sub-types, particularly European outlet centers, top Canadian regional malls, and select open-air centers in the US.

- All-over-the-map office — The office sector is quite literally “all over the map”, with huge variation in outlook depending on geography, ranging from Seoul, South Korea, where office market conditions are currently tighter than nearly any other market/sector combination globally, to the many North American office markets where vacancy rates are well into double digits. We stand by our long-held views13 on the widely varying prospects for global office markets, with Asia-Pacific markets (ex-Australia and China) having the best near-term outlook, US markets having the worst, and Europe in between. One office sector theme that deserves special mention is the increasingly compelling case for investment in super-prime offices in a handful of key European central business districts. We see the conditions for a substantial shortage of top-quality space several markets, which should lead to substantial rent spikes for the best positioned assets.

Other key secular themes driving investment opportunities today include the implications of artificial intelligence (AI) adoption for data center demand, student mobility for student accommodation in Europe and Australia and aging for senior housing.

Don’t wait for the “all clear”

Past experience of real estate cycles suggests that the best investment opportunities tend to arise in periods marked by significant uncertainty, volatility and pessimism, but also when early signs of improvement and stabilization are present—in other words, moments similar to today’s environment. Experience also reinforces that it is nearly impossible to time the market, so it is best to be selectively active throughout the cycle. By the time the “all clear” signal is sounded after a market crisis, it is too late to achieve the best risk-adjusted returns.

That said, “red pill” thinking means we must recognize that the coming capital market rebound is unlikely to be as sharp as it was after the Global Financial Crisis (GFC), given that central banks are unlikely to usher in ultra-loose policy. Seeing the market as it is requires accepting the likelihood that interest rates could remain sticky, and a realistic view of near-term fundamentals as a wave of supply impacts some sectors.

LOOKING AHEAD >

- Strategies for both new and existing investments must take a realistic stance on interest rate uncertainty, with duration exposures aligned to an investor’s goals and risk appetite. Using real estate as a vehicle to place bets on bond markets is as inefficient as it is misguided. We continue to recommend that investors be largely “takers” of bond market signals, and today those are pointing to interest rates remaining high for longer in the US and several other key markets.

- Upended development economics in many markets and sectors means that assets can be bought well below replacement cost, suggesting rents will need to rise and/or land prices will need to fall to justify incremental supply. While buying below replacement cost can be one indicator of a potentially attractive acquisition opportunity, we are cautious about using replacement costs in isolation as an investment decision-making tool. It is essential to adjust for the capital expenditure required to truly equalize the market position of a new asset versus an old one. Often a building is worth less than the cost to build a new building simply because it is old and uncompetitive.

- The anchor of “replacement cost rents” only operates when there is a fundamental need for additional space. In heavily vacant markets, such as US offices, it likely will be years before this mechanism kicks in. Investors acquiring below replacement cost in heavily unbalanced markets must be prepared to wait a long time for that discount to close, and the extended passage of time to monetize a discount is mathematically deleterious to IRRs. A focus on markets working through short-term challenges such as a wave of new supply, but characterized by long-term strength, may generate the best risk-adjusted returns.

- Market bottoms are hard to see in the moment, and only tend to become obvious in retrospect many months down the line; it is hard to see today whether we are fully clear of the lowest point in prices. But we have a least moved from a period of relentless upward movement in rates to volatility around a pivot point. Moreover, challenged capital stacks built before the great tightening still need repair. Both observations point to potentially strong opportunities to invest today across real estate debt and equity.

Footnotes1 Also see our ISA Briefing, “Elections everywhere, all at once: Geopolitics and risk”, April 2024. In that note, we highlighted the various sources of political uncertainty this year and outlined how we recommend investors consider these risks. At the time of writing, political developments are particularly salient for short-term movements markets in France and the UK, given elections that have been called in those countries.

2 Source: MSCI Real Capital Analytics and Trepp

3 Japan and China are key exceptions that we cover in greater depth under the “deciphering divergence” header.

4 Of course, there is considerable variation embedded in this and any assessment of fair value. As always, the devil is in the detail on the assumptions that go into expected and required returns; at LaSalle, specific fair value inputs and conclusions remain a proprietary output.

5 The Merrill Lynch Option Volatility Estimate (MOVE) is a market-implied measure of volatility in the market for US Treasuries. It calculates options prices to reflect the expectations of market participants on future volatility. Observation made as of June 24, 2024.

6 Source: Bloomberg as of June 26, 2024.

7 For more discussion of the Canada-US divergence and the consequences of mortgage rate resets, see our ISA Briefing, ”The impact of residential mortgage resets”.

8 For more detailed discussion of the unique factors in the Japanese and Chinese macro environment, see our ISA Briefing, “Key economic questions for China and Japan”.

9 Source: Oxford Economics; Gavekal Dragonomics as of June 26, 2024.

10 Economic theory suggest that weak currency may contribute to inflationary forces because it pushes up the cost of imported goods.

11 See our PREA Quarterly article on “The Changing Definition of Core Real Estate” for a discussion of how the characteristics considered desirable in core properties is moving from traditional metrics like lease length, to observed qualities like the stability of cash flows. This shift elevates the appeal of niche sectors sub-sectors versus traditional sectors such as conventional office.

12 See our ISA Focus report “Revisiting the future of office”, published March 2023.Important notice and disclaimer

This publication does not constitute an offer to sell, or the solicitation of an offer to buy, any securities or any interests in any investment products advised by, or the advisory services of, LaSalle Investment Management (together with its global investment advisory affiliates, “LaSalle”). This publication has been prepared without regard to the specific investment objectives, financial situation or particular needs of recipients and under no circumstances is this publication on its own intended to be, or serve as, investment advice. The discussions set forth in this publication are intended for informational purposes only, do not constitute investment advice and are subject to correction, completion and amendment without notice. Further, nothing herein constitutes legal or tax advice. Prior to making any investment, an investor should consult with its own investment, accounting, legal and tax advisers to independently evaluate the risks, consequences and suitability of that investment.

LaSalle has taken reasonable care to ensure that the information contained in this publication is accurate and has been obtained from reliable sources. Any opinions, forecasts, projections or other statements that are made in this publication are forward-looking statements. Although LaSalle believes that the expectations reflected in such forward-looking statements are reasonable, they do involve a number of assumptions, risks and uncertainties. Accordingly, LaSalle does not make any express or implied representation or warranty, and no responsibility is accepted with respect to the adequacy, accuracy, completeness or reasonableness of the facts, opinions, estimates, forecasts, or other information set out in this publication or any further information, written or oral notice, or other document at any time supplied in connection with this publication. LaSalle does not undertake and is under no obligation to update or keep current the information or content contained in this publication for future events. LaSalle does not accept any liability in negligence or otherwise for any loss or damage suffered by any party resulting from reliance on this publication and nothing contained herein shall be relied upon as a promise or guarantee regarding any future events or performance.

By accepting receipt of this publication, the recipient agrees not to distribute, offer or sell this publication or copies of it and agrees not to make use of the publication other than for its own general information purposes.

Copyright © LaSalle Investment Management 2024. All rights reserved. No part of this document may be reproduced by any means, whether graphically, electronically, mechanically or otherwise howsoever, including without limitation photocopying and recording on magnetic tape, or included in any information store and/or retrieval system without prior written permission of LaSalle Investment Management.

Jul 01, 2025

PERE: Q&A with Global CEO Mark Gabbay

LaSalle’s Global CEO sat down with PERE to discuss the world’s simplest, most complicated asset class.